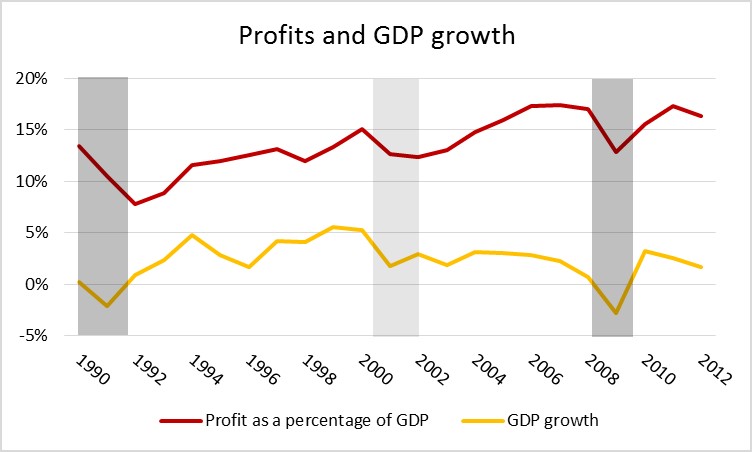

Several weeks ago, I published a series of blog posts on profitability and investment in Canada since the financial crisis of 2007-8. These were republished as a single long article on Socialist Project and given the title, “Canada’s Profitability and Stagnation Puzzle”. Since them, Sam Gindin has published a reply to my piece, “Puzzle or Misreading? Stagnation, Austerity and Left Politics”. Gindin challenges me on a number of fronts, most generally for misreading the current predicament in terms of a static formula that treats all capitalist crises ahistorically. This critique has ramifications for how Gindin sees not only my empirical account of present trends, but also my theoretical background and thoughts on strategies for resistance and alternatives.

Despite what appear to be many points of dispute, I think Gindin and I actually agree on a great many things, both in terms of the diagnosis of the current crisis and strategies for overcoming it. There are quibbles about statistics and wording, and I want to deal with a couple of these here, but I think we share much on broader theoretical and strategic matters. I want to primarily focus on the agreements behind our recent Socialist Project-facilitated interaction.

{kind=link}