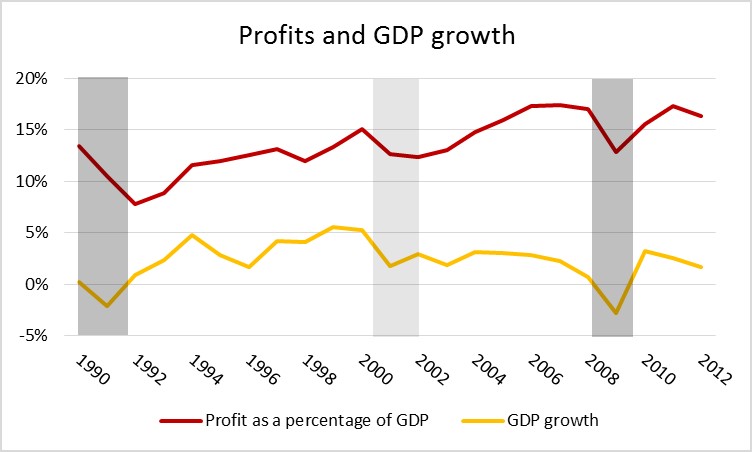

In my previous post, I outlined the disconnect between profitability and investment in Canada’s private sector. While businesses are doing well and profits have rebounded quickly after the global financial crisis of 2007, investment has continued its slow and steady 20-year decline. This decline is especially visible when investment is related directly to profits. Slightly more than 60% of gross profits are currently being re-invested, down by a third relative to just two decades ago. Such a gap between strong profitability and dismal investment does not correspond with standard accounts of how the economy functions. According to standard accounts, strong profitability should encourage investment, not depress it further. This theoretical relationship is not borne out in recent Canadian experience.

While the last post also examined a few factors that could have been at play in creating this odd state of affairs, here I want to move in the opposite direction and look at two competing pictures of how to revive low private-sector investment. The first picture comes from Keynes, the second from Marx. I am particularly indebted to Michael Roberts, who has written extensively on the crisis from a UK perspective and who used a similar framework in a recent article (on the adoption of the idea of a permanent slump by mainstream Keynesians).

The two pictures agree on a diagnosis of on-going stagnation – with low investment being just one feature. Indeed, the lack of sustained recovery across much of the developed world has led increasing numbers of mainstream economists to declare that the current slowdown is permanent. Paul Krugman, likely the most prominent Keynesian economist, recently wrote that we may have entered a “permanent slump.” Even the more hawkish Larry Summers has added his voice to the chorus, referring in a recent speech at the IMF to a period of “secular stagnation”. Many Marxist and other radical economists have, of course, been making the same point for years, citing a variety of structural changes and imbalances in the economy, particularly those that characterize the neoliberal period that began in the 1970s when the great post-war boom lost steam.

While their diagnosis may be similar, Keynesian and Marxian economists see the way out of the current long-term slump rather differently.

{kind=link}