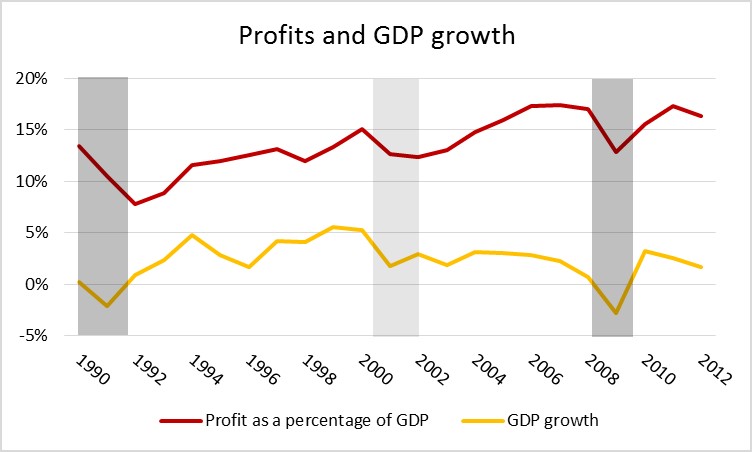

This is the third and final post in what has become a three-part series on the puzzle of high profitability and low investment in the Canadian economy. In the first part, I looked at some data that shows the existence of the puzzle and explored a few of the factors that could be behind it. The follow-up post outlined broadly Keynesian and Marxian solutions aimed at raising investment: the former based on stimulating demand, the latter on eliminating overcapacity and increasing the relative profitability of productive capital. Here, I want to continue the thoughts that concluded the second part, namely that the Harper government’s preferred response to the puzzle has been neither demand stimulation nor industrial policy. Instead, it has been austerity – a strategy by no means accidental, but in fact designed to support the status quo of high profitability and low investment.

Austerity is not an isolated Canadian phenomenon nor is it a new one. The neoliberal era that began sometime in the 1970s has seen austerity in one form or another applied worldwide. Economic crises have especially provided governments with excuses to institute or continue austerity policies that would not have been difficult to institute otherwise. While Canada did not experience the latest economic crisis to the same extent as a number of other countries, it has seen a more moderate version of many of the same trends – such as slower growth and lower employment. The crisis was large enough to allow the Harper government to continue and deepen a tentative austerity regime. While Canada has not pursued austerity programs as spectacular as some, for example the UK or Spain, the Conservative government has, nevertheless, succeeded in substantially reducing the size of government, small cut by small cut. While Canadian austerity policies predate the crisis, the crisis has only helped to entrench them and further orient them towards propping up profitability.

{kind=link}